The competitive landscape for talent is fierce and has intensified with the impact of the “Great Resignation.” In unprecedented numbers, U.S. workers are actively seeking employment arrangements that work for them and are commonly incentivized by not being bound to a daily commute and mandatory office working.

Two years on from the COVID-19 pandemic first reaching the U.S., the world of work is permanently changed -- hybrid working arrangements are widespread and the norm across many industries.

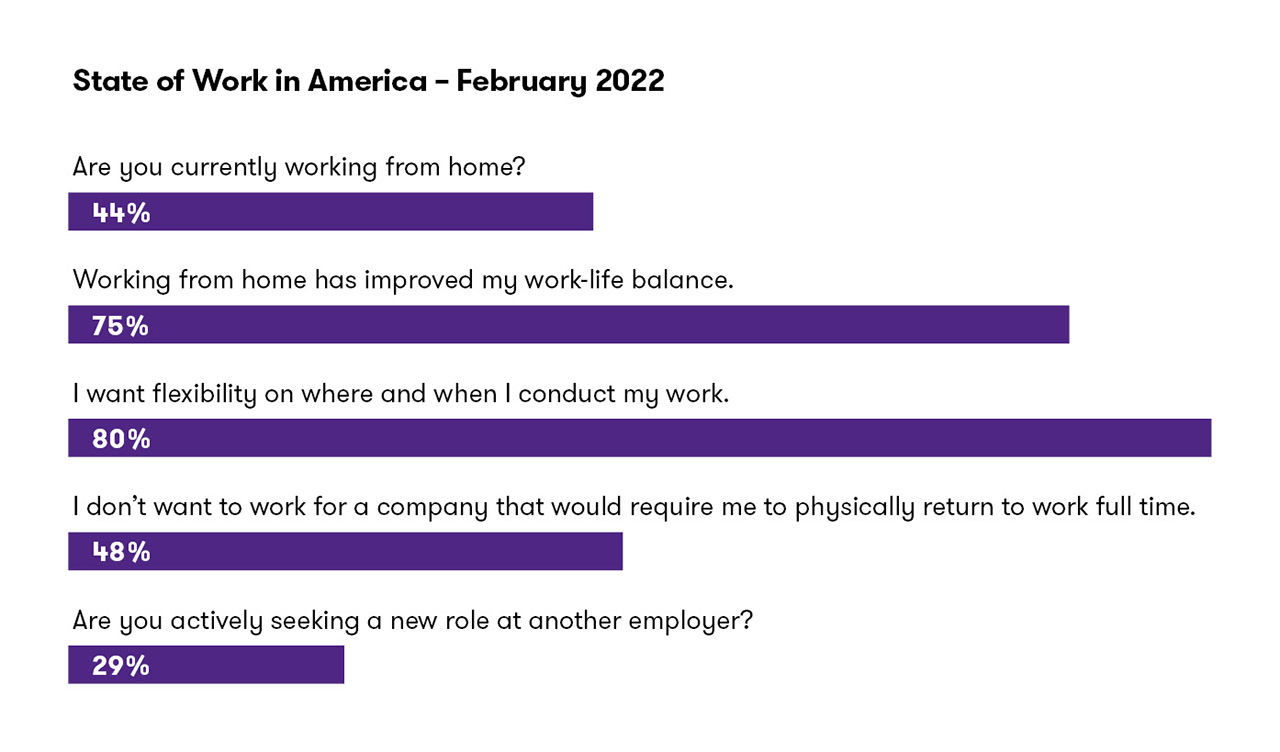

Grant Thornton’s February 2022 State of Work in America report provides insights into the transformed landscape for employees across the country.

Employers, too, are operating in new ways, such as taking a “borderless” approach to hiring as geography becomes less relevant for finding the right talent.

These ongoing challenges and changes in the labor market can, however, present opportunities for companies to access and retain the talent they need to grow. The search for talent has moved quickly beyond geographic restrictions – U.S. employers are now hiring across the U.S. and for many, the search for the best talent has them searching outside the U.S., too.

Finding the right international path forward

As workforces become international with the addition of new hires overseas, employers face the challenge of how to approach the range of complexities, costs and risks these scenarios can present, such as immigration, employment law and taxes. Understanding the responsibilities and obligations both employers and employees assume with these arrangements is key to the long-term effectiveness, competitiveness and success of international hiring.

Adding a new U.S. hire living and working outside the country presents a breadth of tax challenges employers must address:

- Corporate Tax – Regardless whether the company has a local corporate entity, a new U.S. hire working remotely in another country could create a corporate taxable presence (or a “permanent establishment” – PE - in countries where the U.S. has concluded a double tax treaty) bringing corporate income tax and compliance obligations.

- Employer Taxes – These may involve an obligation to register with the tax authorities, operate a payroll, calculate and remit taxes in a foreign country where the new employee resides. Additionally, exposure may arise to overseas employment taxes and social security contributions.

- Employee Tax - An employee’s tax arrangements may differ in having a U.S. employer rather than a local one in the country they reside and bring unexpected or burdensome new obligations.

Below we discuss seven approaches to engage and hire new talent outside the U.S.

1. The U.S. company registers overseas

With a global talent market to target, U.S. employers may find the right candidates in countries where they do not have a local company and their global footprint expands as hiring goes international.

In reviewing the tax implications of such arrangements, the starting point should be to determine whether the new hire’s remote working arrangements could create a taxable presence for the U.S. company. This has the potential to drag U.S. profits into taxation in the foreign country where the employee works, and where the requirement lies to register and file tax returns. This in turn can trigger U.S. tax ramifications and compliance obligations. Alternatively, and depending on factors including the volume of new hires in a country, the U.S. employer could create and register a new corporate entity in the overseas country, similarly triggering local compliance and filing obligations.

In either situation, local regulations are likely to require payroll be operated where applicable, taxes withheld and where local employer and employee social contributions are paid. The cost of these contributions, which in some European countries can reach 50% of income, should be quantified. Statutory benefits will also need to be understood, along with benefits that are customarily provided in the local market.

Though there’s tax complexity in addition to the broader considerations when establishing a presence in a new country, a local presence provides the framework for increased hiring and the ability to go toe-to-toe in the local talent market with key employee expectations around benefits and payroll compliance.

2. Hire the individual into the local company

Where the U.S. company is registered as an employer in the overseas country, it may be possible to hire new employees into that company. In being hired as a local employee, an individual will have employment arrangements in line with the rest of the market, for example, access to local benefit plans, payroll tax withholding, and remuneration paid in local currency. Convenience, ease of administration and competitive terms mean this may be an effective approach for an employer.

If the new hire is in fact working for the U.S. company, this can present risk of creating a taxable corporate presence. .Though each new hire cases should be considered based on the facts, the following situations may present risks depending on how the local tax authorities approach this.

- The employee can and does negotiate and/or sign contracts on behalf of the U.S. company.

- The employee is active in business development in the local market on behalf of the U.S. company.

- Their physical working arrangements, such as having an office, may be regarded as a “permanent place of business” for the U.S. company.

- Their role is part of the core business of the U.S. company.

3. The new hire takes on the compliance obligations

There may be countries where corporate and PE risk for the U.S. employer is limited and there may be no obligation to register and operate a local payroll. There may be differences in how the lack of payroll obligations arise and in this circumstance it’s important to also understand the impact on the employee and the administration burden that employee may need to take on in comparison to a regular employee of a local company:

- Obligation defaults to employee – Payroll registration may be optional for the U.S. company and where no action is taken, reporting, calculation and remittance of taxes may default to the employee. In some countries, like Hungary, the employer’s social security obligations may also be levied on the employee, increasing their tax burden.

- Employee required to meet compliance obligations – Alternatively, local tax regulations may require the employee to operate a particular payroll or compliance regime to ensure timely tax payments are made. The UK’s PAYE direct payment scheme, for example, requires the employee to operate a payroll scheme where there is no local employer, including meeting the strict timeframes for reporting (known as Real Time Information).

Employers may choose to provide tax assistance to help an employee to meet the tax requirements locally. However, if the obligation presents itself, there is a potential for the employee to incur additional costs or taxes that other local employees may not face.

4. Hiring a contractor instead of employee

Where a company does not have a presence in the country where a new employee resides, or where the local entity will not hire them, it may be tempting to engage as an independent contractor rather than employee. There can be a misperception that an independent contractor does not carry the same tax compliance and cost exposure to a U.S. company as if they were hired as an employee.

The substance of the engagement is key in determining whether a contractor arrangement is appropriate, or whether there is, in effect, deemed to be an employment arrangement with the individual. Much as the IRS assesses a 20-factor test in determining employment status, weighing the subjective considerations to determine whether a deemed employment exists, many countries apply very similar criteria and tests. Factors commonly reviewed for this determination include the degree of integration into the business (e.g. Do they have a company email or phone number? Are they integrated into the business effectively like an employee?), who directs and “controls” the work they undertake, whether they have financial exposure for the services they perform, and how they are remunerated (fixed fee or in effect, salary, as well as provision of employee benefits).

For a U.S. company engaging contractors overseas, there may be risk that foreign tax or labor authorities could undertake an audit and make a determination that contractors should be regarded as employees. Additionally, in some countries, the employee may take legal action to be treated as an employee. This opens the company up to corporate and PE exposure, employment taxes, penalties and interest, and potentially employee tax liabilities for not operating payroll withholding. While appropriate for many arrangements, careful consideration and review should be undertaken for international hiring.

5. Use a professional employment organization

An employer may choose to engage a third-party professional employment organization (PEO) to employ an individual. The employee is then leased back to the company for a fee. This arrangement allows the PEO to take on the legal, tax and payroll compliance burdens on behalf of the U.S. employer. Offering a quick, albeit potentially more expensive, solution, PEOs may provide interim or even long-term hiring solutions in countries where the company may have a low headcount of new hires and does not want to create a new entity or register a PE.

Though a streamlined approach for the employer, consideration should be given to both the possible tax risk to the company as well as the employee experience using a PEO. Corporate tax risk may not be ringfenced by having a third-party company act as the employer in place of the U.S. company. Countries including the Netherlands and China for example will look at subjective factors such as 1) the employee’s role and responsibilities, 2) where they report into, 3) if their work is directed from the U.S. and 4) where economic benefit is derived, to determine whether the U.S. company has created a taxable presence.

An employee working via the PEO also may not have access to company benefit and incentive plans. These cultural and remuneration considerations will be important factors for many U.S. employers in deciding whether such an arrangement is appropriate.

6. Whether to embrace “digital nomads”

Countries such as Costa Rica, Romania and Greece are embracing the ability to work from anywhere with the introduction of “digital nomad” visas. These visas allow individuals to reside in the country for an extended period without more complex visa sponsorship requirements. While attractive to employees and the self-employed alike, these arrangements often do not include any provisions that exempt an individual from becoming liable to income and social taxes. Similarly, there may be no protections for the employing company, meaning new hire employees working overseas with such an arrangement could expose the company to corporate and employer taxes in addition to reporting and other compliance obligations.

“With several global destinations legislating in the area of digital nomads and subsequently creating work and residence authorizations for these alternative employment arrangements, there can be no question the number of people working remotely outside their home country will continue to climb,” said Dan Morris, director and counsel at Newland Chase. Care should be taken to understand each country’s program and whether it is viable from a tax perspective.

7. Do nothing

As a last option, employers could choose to take no actions, recognizing there is inherently risk in not quantifying or understanding potential exposure. The question as to who has the responsibility to manage taxes in a foreign country often results in an answer that both the company and employee have exposure and obligations. If employees meet their obligations, file returns and pay taxes, the U.S. employer who chooses to take no actions in the foreign jurisdiction may be visible to the foreign country tax authorities, accruing potential risk and exposure to a local entity or to future operations if they have not yet set up there.

Importantly too, this could create unexpected and costly pitfalls. For instance, New York’s “convenience of the employer” rule may expose a new hire whose office and main place of business is there to New York’s state income tax, even if they are hired overseas and choose to remain working overseas.

Threading the needle of compliance

Companies need to recognize there are multiple paths forward and often, no “right answer” on how to hire employees overseas. Rather, there may be compromises to meet tax and legal compliance obligations, provide a remuneration and benefits package that’s competitive, and balance the burdens and costs this can place on both a U.S. company and an employee. Whichever approach employers take, going global in the search for talent can bring the competitive edge they need in a challenging market.

Contact:

Richard Tonge

Principal, Global Mobility Services Practice Leader

Richard is a Principal in our New York Human Capital Services practice and leads the Global Mobility Services practice in the United States.

New York, New York

Industries

- Technology, media & telecommunications

- Retail & consumer brands

- Manufacturing, Transportation & Distribution

- Media & entertainment

Service Experience

- Tax

- International Tax

- Human Capital Services

- Global Mobility Services

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information. Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “Section,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

More human capital bulletin

No Results Found. Please search again using different keywords and/or filters.