You’ve heard of cryptocurrency, but should you accept cryptocurrency donations?

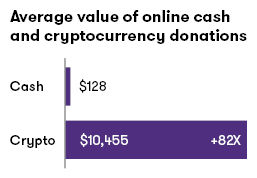

A growing number of donors are offering donations in Bitcoin, Ethereum and other cryptocurrencies. One cryptocurrency donation platform, The Giving Block, reported that it processed more than $69M in 2021. Plus, cryptocurrency donations were larger — averaging $10,455 each, versus $128 for the average online cash donation.

Donors are typically subject to a capital gains tax if they convert a cryptocurrency to US dollars or another currency to donate. They can typically avoid this tax by donating cryptocurrency directly. Then, when itemizing their taxes, they can still claim a charitable donation for the cryptocurrency’s value at the time of the donation.

Cryptocurrency values can be volatile, but their overall popularity — and their use for donations — are likely to keep growing. That’s why more not-for-profit organizations are establishing ways to accept and manage these donations. Before organizations accept cryptocurrencies, it’s important for them to understand a little about the technology, potential risks and the best ways to prepare.

If you’re not familiar with the blockchain technology behind cryptocurrencies, it’s best to begin with some quick background on how it works and why it matters.

What is blockchain?

How it works: A blockchain is a distributed database that serves as a digital ledger of transactions between accounts (electronic address). Each transaction records the accounts involved and the amount. The database is distributed, in that duplicate copies are stored on computers that form a network. These copies are called “nodes” and are equally authoritative about the transactions — each node can independently validate a group of new transactions in a “block.” When a significant number of nodes validate the transactions in a block, the nodes confirm and finalize the block. If one node submits an unauthorized or invalid block, the other nodes in the network will reject it. Once transactions on the ledger (blocks on the chain) are confirmed and finalized, they can never be edited — only added to, with new transactions.

Why it matters: The main advantages of blockchain technology are its resilience and reliability. A blockchain network is resistant to disruption because its nodes operate independently and are equally authoritative — if one node goes offline, the blockchain still functions. A blockchain network is reliable because a block of transactions cannot be undone or reversed after it is confirmed and finalized.

Blockchain technology manages digital assets, like smart contracts, non-fungible tokens and cryptocurrencies. While the technology can be very secure, there are still some risks.

What are the risks?

Even if your organization does not hold any cryptocurrency, you might encounter people who want to donate them. The ability to accept these donations could accelerate and broaden donations from your fundraising activities, but there are some risks to consider:

- Volatility:

The values of cryptocurrencies shift more than most traditional government-issued (“fiat”) currencies like the US dollar. - Universality:

Some of the less-popular cryptocurrencies have limited markets for trading them, which can present a challenge for exchanging them to other currencies. - Regulation:

The laws regulating cryptocurrencies still lack coordination and consistency among some jurisdictions, which can raise uncertainty and compliance costs. - Security:

Cryptocurrency systems can be at a higher risk of being targeted by hackers, malware, ransomware and fraudsters. - Insurance:

Cryptocurrency holdings can be difficult to insure. If uninsured holdings are lost from a hack or a lost password, they might be unrecoverable. - Substantiation and tracing:

Since cryptocurrency transactions only record account numbers for participants, they can be anonymous. That can make it difficult to establish and substantiate the true source of a cryptocurrency donation. If a cryptocurrency donation is found to originate from criminal activity, the recipient might need to return the donation.

These risks can sound intimidating. However, transactions in US dollars or any other currency come with risks as well. As with those transactions, you can use established guidelines to help you mitigate the risks.

What are the guidelines?

For the most part, not-for-profit organizations are allowed to hold cryptocurrencies as investments, to transact with customers or for other purposes, and generally follow the same guidance as for-profit entities. However, there are some differences. You can find specific cryptocurrency guidance in some of the following:

- Association of International Certified Professional Accountants (AICPA):

The AICPA’s Accounting for and auditing of digital assets advises organizations to consider risks as they update their gift policies, train staff, and ensure their internal controls address the valuation and processing of cryptocurrencies. Organizations should also understand how to report the related transactions, balances and disclosures within their financial statements. The AICPA has also published other guidance on accounting for blockchain. - Financial Accounting Standards Board (FASB):

If you receive a cryptocurrency or another type of digital asset as a donation, it should be measured at fair value on the date of the donation. Then, subsequent accounting depends on how you use the assets. If you hold it as an investment, ASC 958-325 and 954-325 provide guidance on accounting for investments in nonfinancial assets acquired for investment purposes. Otherwise, account for it as an intangible asset. The fair value of the asset at the date of the donation becomes its carrying value for the purposes of subsequent measurement. So, make sure you understand the relevant guidance that is specific to what your organization decides to do with the assets. - Internal Revenue Service (IRS):

The IRS’ Notice 2014-21 explains how to treat digital assets for federal income tax purposes. It indicates that, for federal tax purposes, virtual currency is treated as property. The general tax principles that apply to property transactions also apply to transactions using virtual currency. The character of the gain or loss generally depends on whether the virtual currency is a capital asset in the hands of the taxpayer.

For tax considerations, the receipt of cryptocurrency is treated no differently than any other type of non-cash donation that the organization receives. Cryptocurrency contributions are reported as revenue on Form 990, at fair value on the date of the donation. You are required to disclose the donation on Schedule B (which is redacted from public scrutiny) and on Schedule M, where non-cash gifts are inventoried. When an organization receives a cryptocurrency donation valued at $250 or more, it must provide a contemporaneous written acknowledgment to the donor. The donor is required to complete Form 8283 for non-cash charitable donations, and obtain a qualified appraisal for deductions more than $5,000. The not-for-profit must sign the donor’s Form 8283 to substantiate receipt of the non-cash gift. It does not mean that it agrees with the appraised value; rather, the not-for-profit is simply acknowledging receipt of the assets on the date specified. Finally, if the not-for-profit sells, exchanges or disposes of the cryptocurrency donation within three years after originally receiving it, it must file Form 8282 (Donee Information Return), providing a copy to the donor.

The IRS published an FAQ on Virtual Currency that addresses many other tax-related considerations.

How can you prepare?

There are primarily two ways you can prepare to accept cryptocurrency donations:

- Collaborate with a service provider:

There are many service providers that help not-for-profit organizations process cryptocurrency donations. For instance, BitPay is a cryptocurrency payment processor and clearing business that will convert donations into US dollars. The Giving Block is a full-service provider that will accept cryptocurrency donations on your behalf, then either convert them to US dollars or hold them for you. Service providers can come with costs, but they can minimize some of the administrative burden and risks involved in handling cryptocurrencies. - Set up in-house capabilities:

Your organization can set up its own digital wallet, with a unique “private key” for access. The wallet lets your organization receive, hold and send cryptocurrencies through its account. Having your own wallet could be more secure, but it also gives your organization an administrative burden without the support and other benefits of a service provider.

Apart from establishing a method for accepting cryptocurrency donations, consider some of the following actions and internal governance policies:

- Review and update your gift acceptance policy:

What does your organization’s current gift acceptance policy say in relation to “Non-standard Contributions”? - Plan your holdings:

If you accept cryptocurrency donations directly, which currencies will you accept? Will your organization immediately convert cryptocurrencies and other digital assets to a fiat currency like the US dollar, or hold it for investment or a program like a museum with a digital art portfolio? - Align to your mission:

Do digital assets align with your mission? For example, cryptocurrency transactions on a proof-of-work network might use large amounts of fossil fuel energy for validation. What other considerations might support or detract from your mission? - Establish risk management:

Do your stakeholders and staff understand the risks, and do you have appropriate risk management in place? For instance, make sure that you provide and update relevant training. - Maintain compliance:

Maintain an awareness of the latest audit and tax guidance, with a plan to update and maintain ongoing compliance activities.

Don’t keep donors waiting

It takes time to effectively prepare for the technology, opportunities, risks and regulation of cryptocurrency donations. If you plan to prepare when you meet your first cryptocurrency donor, you’ll probably be too late. You don’t want to have to tell a donor “no,” or even “wait.”

So, now is the time to prepare. Document your plan in your gift acceptance policy, and involve your board in that discussion. Make sure to discuss the changes and risks, documenting decisions and approvals. Then, make sure you have technology, accounts, policies and procedures in place. Prepare to accept, secure, account for and disclose cryptocurrency donations.

Once you are prepared, you can foster donor relationships with the confidence, flexibility and freedom to plug into a powerful outlet of support.

Contacts:

Markus Veith

National Leader, Blockchain, digital assets and Web3 solutions

Partner in charge of the Northeast Financial Institutions Practice

Markus leads Grant Thornton’s Digital Asset Practice and is the Partner-in-charge of the Northeast Financial Institutions Practice and an SEC and IFRS specialist. Markus has over 20 years of experience in the financial services industry and in public accounting.

New York, New York

Industries

- Construction & real estate

- Asset management

- Banking

- Private equity

Service Experience

- Strategic federal tax

- Tax

- Advisory

- Audit & Assurance

- Restructuring and turnaround

- Valuation

- Employee Benefit Plan Audits

Rahul Gupta

Partner, National Professional Standards Group

Rahul is a Partner in the National Professional Standards Group (NPSG) of Grant Thornton LLP. Rahul assists engagement teams and clients with technical accounting issues and monitors current accounting developments, under both U.S. GAAP and IFRS.

Chicago, Illinois

Industries

- Construction & real estate

- Manufacturing, Transportation & Distribution

- Technology, media & telecommunications

- Energy

- Retail & consumer brands

Service Experience

- Audit & Assurance

Yossi Jayinski

Partner Audit Services, Not-for-Profit and Higher Education

Leader, Jewish and Israel Organizations Sector

Yossi Jayinski has more than 17 years of public accounting experience serving a variety of industries, including the financial services industry. He has performed audits of private and public companies, as well as various IPOs, and has served as an adviser for U.S. and international businesses.

Iselin, New Jersey

Industries

- Healthcare

- Technology, media & telecommunications

- Not-for-profit & higher education

- Asset management

Service Experience

- Audit & Assurance

Scott Thompsett

Managing Director, Tax Services

Scott has over 23 years of experience in the higher education and not-for-profit industry and has been a member of the Grant Thornton Not-For-Profit practice for five years.

Long Island, New York

Industries

- Healthcare

- Not-for-profit & higher education

Service Experience

- Tax

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information. Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “Section,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

Our not-for-profit and higher education featured industry insights

No Results Found. Please search again using different keywords and/or filters.